For beginners learning to invest their own money in Singapore, it is beneficial to keep track of the company’s financial performance. This allows you to make a decision as to whether you want to continue being invested in the economic future of a particular company or will wish to divest and seek other opportunities. Having a clear understanding of what the company does will also help you assess future threats such as the impact of the recent spreading of the Corona virus in Singapore and around the world.

Outlook

Mapletree Logistics is a logistic reit with a diversified portfolio across various geographies; Singapore (37.4%), Hong Kong (25.9%), Japan (10.2%), China (5%) and others. With the ongoing US China trade tensions, the Hong Kong Protest and Corona Virus, it has been difficult for Mapletree logistic’s customers to accurately anticipate their future need for logistic space. The increased macro uncertainty has hit Mapletree Logistics as it is focused in geographies that are most impacted by these negative developments.

Revenue and distributions

Gross revenue for 3Q 2019 was 121.148 million. Relatively to 3Q 2018, revenue growth was relatively flat at 0.29%. However, net income was higher at 108 million. This was a result of lower property expenses as well as gains from several property divestments. These gains were spread out as partial distribution across various quarters. Divested properties includes Gyoda Center, Iwatsuki B centre, Atsugi Centre and 7 Tai Seng Drive. Apart from divestment of properties, Mapletree logistics also divested its wholly owned subsidiary Mapletree Log Integrated Shanghai.

All in all, MLT performed well for 3Q 2019 and paid out a distribution of 80.8 mil, approximately 6% higher than in 3Q 2018. However, not all of the distributions are paid to unit holders. 4.29 mil was paid out to perpetual securities holders.

Financial position

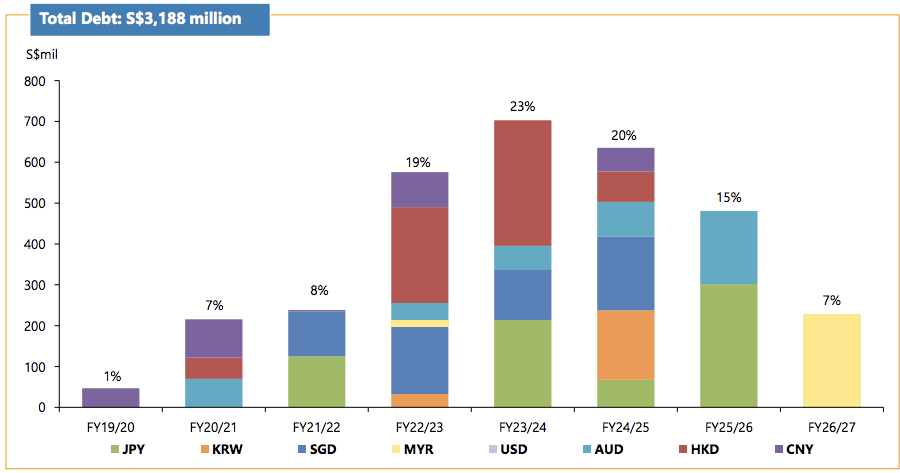

MLT has maintained a strong cash position of around 223 million and a relatively low debt to asset ratio of 36.2%. If the debt from joint ventures and subsidiaries are included, leverage will increase to about 37.5%, which is well below the 45% regulatory mark, giving ample headroom for the Reit. With a cash flow from operations of 134 million from 3Q 2019 as well as cash equivalents of 223 million, MLT can repay the 365 million of unsecured borrowings due in the coming year. Looking ahead, the 7-8% that needs to be refinanced in FY 20/21 and FY 21/22 remains fairly manageable for the reit.

Portfolio Performance

Amidst uncertainty , MLT’s properties continue to show relative resiliency with occupancy at 97.7%. Rental reversion has remained positive at 1.2% and the Weighted Average Lease Expiry (Wale) was around 4.4 years.

Conclusion

Like other reits, Mapletree Logistics Trust is likely to post weaker operating results as it faces the headwinds from recent global developments. However, as a logistic reit, it should be less impacted as compared to other reits such as Capitaland Mall Trust which will be directly affected by the sharp drop in shopping traffic due to the development of the corona virus