Recent Updates

Brief Introduction

Interested in investing in Singapore Office Properties? As you learn about investing your money in Singapore, you would have come across Capitaland Commercial Trust, CCT for short. CCT was first listed on 11 May 2004 and focuses on Grade A Office Properties in Singapore. These properties include the likes of Capital Tower, Asia Square 2, CapitaGreen and 21 Collyer Quay.

However, what if you do not want to be invested in Capitaland Commercial Trust will still like to get some exposure to the office space? Or perhaps you already have exposure to Capitaland Commercial Trust and wishes to get some diversification. If these are your concerns, then you should take a look at Keppel Reit.

Keppel REIT was listed 2 years later than Capitaland Commercial Trust. Although it is smaller, it owns quite a few premium Grade A commercial assets. Its objective like all reits is to generate stable income and long term growth for its unit holders.

Below is a Stock Chart for Keppel Reit.

History of Keppel Reit

Keppel Reit was first floated in 2006, at a time when the entire REIT Industry was experiencing fast growth. In that year alone, 8 Reits got listed on the local stock exchange.

Keppel Reit is sponsored by Keppel Land, the 100% subsidiary of Keppel Group. Its initial portfolio in 2006 included Prudential Tower (approximately 44.4% of the strata area of the building), Keppel Towers, GE Tower and Bugis Junction Towers. The initial portfolio value had a net lettable area of 73,108 sqm, 100% occupancy, and a valuation of around 677 million. Since then Asset under management has grown to about 8.9 Billion.

Difference between Keppel Reit and Keppel

Many Singaporeans when looking at a REIT like Keppel REIT will ask this question. “What is the difference between Keppel Reit and Keppel?” After all, Both companies have the word Keppel in their name. While we covered the same topic in Capitaland Mall Trust Dividend Share Price Company Analysis, it is a good idea to recap and also cover something new about the trust structure of Keppel Reit

If you look at the trust structure of Keppel Reit, you will realise that Keppel is not there. The reason is because, Keppel is one of Keppel Reit’s unitholders. Keppel owns an approximate 47% of Keppel Reits’s units, with the majority of the remaining units being left as public float. This means that it is the public who is the majority owner of Keppel Reit.

Despite not owning the majority of Keppel Reit’s units, Keppel continues to have management control of Keppel Reit. This is because Keppel Reit Management Limited, the manager of Keppel Reit, is the wholly owned subsidiary of Keppel.

In addition, Keppel’s wholly own subsidiary (Keppel Land) is also the sponsor of the Reit.

Valuation First, Business profile second

There are many valuation techniques that we can use to judge the attractiveness of a potential investment. These can range from

- Stock Price V.S NAV Per Unit

- Dividend Yield V.S Net Property Yield

- Dividend Yield V.S comparable opportunities

- Management’s own Investment Hurdle

- Potential for Strong Rental Reversion

- Potential for Further Cap Rate Compression

Stock Price V.S NAV Per Unit

Given that a REIT is in some sense its portfolio of properties, some will argue that a fair value to pay for a single shareholding is the NAV per unit. The NAV is calculated by first taking total assets and deducting by total liabilities. This will include the subtraction of both long term and short term debt. There after, the NAV is deducted by the total number of units outstanding to arrive the NAV per unit. For Keppel Reit, as of 2019, the NAV per unit is 1.35

Given that Keppel Reit has historically traded in the SGD 1.2-1.3 range, its a sign that market sees the Reit as fairly stable with minimal room for further cap rate or yield compression.

Dividend Yield V.S Net Property Yield

Apart from looking at NAV per unit, one can also compare the dividend yield with the net property yield. How do you derive both numbers and what is the difference between the two? The dividend yield is what the management has announced it is going to distribute for the quarter or year, divided by the price of the security. This number is therefore:

- Subject to a certain degree of management discretion (do note that management has to pay 90% of distributable income)

- Includes the effect of the firm using leverage

It is derived as follow:

| Period | Cents |

| 1 Oct 2019 to 31 Dec 2019 | 1.4 |

| 1 Jul 2019 to 30 Sep 2019 | 1.4 |

| 1 Apr 2019 to 30 Jun 2019 | 1.39 |

| 1 Jan 2019 to 31 Mar 2019 | 1.39 |

| 5.58 |

Keppel Reit is currently trading at SGD 0.98 (as of 17 March 2020). Given the distribution table as shown below, the distribution yield should be around 5.6%. This means that if you were to buy a unit of Keppel Reit now and the distribution remains constant at 5.58 cents, your return from annual distributions will be 5.6%.

However, do note that the price of SGD 0.98 cent is a result of macro uncertainty and high market volatility. Hence, the dividend yield that can be achieved will fluctuate depending on the entry level that investors have chosen.

Meanwhile, the Net Property Yield is the total income that is derived from the Property minus any related expenses.

| FY19 (mil) | |

| Net Property Income | 128.9 |

| Investment Property | 3730 |

| Investment Property Yield | 3.46% |

As of FY 2018, the property yield for Keppel Reit will be around 3.46%. Given that the current dividend yield is at 5.6%, the share is considered attractive as it is yielding more than it would have if you bought the entire portfolio at 3.7 Billion and produced a 3.46% Net Income Yield.

Further, the 3.46% yield is considered a high estimate as it includes the income from associates but did not include the 2 Billion of investment in associates.

Dividend Yield V.S comparable opportunities

Some may argue that this level of dividend yield is attractive relative to other assets. As of this writing, this is still higher than the 2.5% you get on your CPF Ordinary Account and also higher than the 10Y SIGB bond yields 2% and lower.

However, 5.6% seems low relative to Mapletree Industrial Trust’s dividend yield of 5.8% (as of March 2020). Given thats the case, should you then maximise your gains by solely buying into Mapletree Industrial Trust? The answer to that lies in whether there is any merits in diversifying your holdings in Reits.

It is worth noting that irregardless of how much you diversify your reit holdings, it may not help you to weather extreme market volatility. This is because when market gets volatile, the correlation across all asset classes tend to go to 1.

Management’s own Investment Hurdle

One good measuring yardstick is to look at the valuation assumptions that the company made in valuing the investment properties. The valuation assumption includes the capitalisation rate that the reit uses. It will also include the discount and terminal rates that are used in valuing the property.

| Valuation tool | 2018 | 2017 |

| Capitalisation Rate | 3.60% – 5.25% | 3.75% – 5.63% |

| Discount Rate | 6.00% – 6.80% | 6.25% – 7.00% |

| Direct Comparison Method | $600/sf – $8,200/s | $600/sf – $8,200/s |

Capitalisation Rate, also know as cap rate is the ratio of Net Operating Income and Market Value. So if net operating income stays the same, it will seem that the assets are already at their full potential.

Why should cap rate mean anything to the Reit Investor

With your dividend yield from holding the REIT being slightly higher than cap rate, it seems to suggest that at the very least, the current stock price is fair. Noting that since dividend yield is the total annual distribution divided by stock price and cap rate is the total net operating income divided by the current market value of the properties, dividend yield for the portfolio will only be higher than the cap rate for individual constituent properties if either

- The REIT has been paying out too much dividend (i.e. more than its distributable income)

- The stock is valued at less than the investment property portfolio

- The cap rate has compressed to a point where management may consider locking in the capital gains by recycling the asset and buying into higher yielding asset.

To verify which scenario it is, one has to track the company and know both the quality of the management and the properties that the Reit owns.

Further Cap Rate Compression

Is it possible to get further cap rate compression in the Grade A Office space?

While we believe there will be little upside, things are never quite certain in finance and hence it is important to run though a series of thought scenarios and probable events that can bring CCT above current prices

- Further compression in market cap rate (Macro)

- Rent reversion => NOI increase => Share Price increases while Div Yield stays constant.

- Accretive Acquisitions

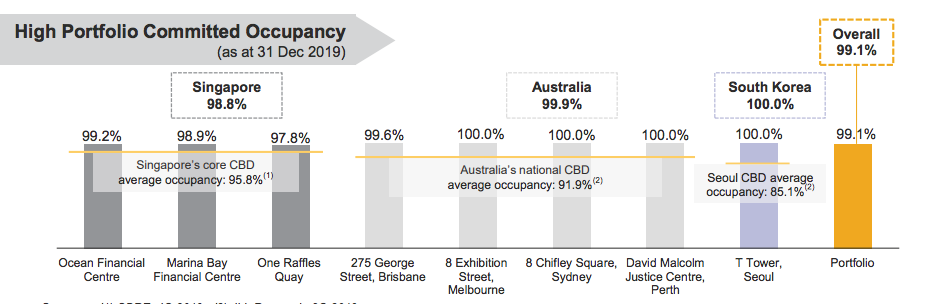

Properties under Keppel Reit

While Keppel Reit’s property portfolio is predominantly in Singapore, it also has a sizeable investment in Australia (15.7%) and Korea (3.8%).

Many of these properties will be familiar to those who work in the CBD. However, do note that for the Marina Bay Financial Centre and One Raffles Quay property, Keppel Reit only has a 33.3% interest in them.

In recent years, Keppel has also moved out of Singapore to look at overseas opportunities in Australia and South Korea.

Thoughts on the properties

There is no doubt that the properties that Keppel Reit holds are high quality Grade A Offices. Beginners learning how to invest their money in Singapore has the benefit over the last year of seeing how Reits can get exposed to macro events that are not within their control. Take Mapletree North Asia Commercial Trust for example. The protest in Hong Kong severely disrupted the operations of Festival Walk which was a Grade A Retail/ Office Development that accounted for more than 60% of net property income.

As investors we may not be able to be fully aware of macro events that can negatively disrupt the performance of our reit investment. Hence, it is important that we choose reits that have a diversified source of income. Keppel Reit does well in that regard with less than 35% of total net property income from any single property.

Just as it is important for the REIT to have a diverse source of income, it is also important that the individual assets perform well. This is often measured by the same store reversion rate as well as the occupancy rate. Keppel has managed to maintain almost full occupancy for its properties in all three countries.